Finance Automation ROI: What Australian CFOs Should Actually Measure (With Benchmarks)

Ordron34 min read

Most finance automation business cases die before they reach the board. Not because the technology is unproven, not because the savings aren't real, but because the person building the case measured the wrong things or measured nothing at all. They projected labour savings from a vendor's slide deck, skipped the baseline, and handed up a number that nobody trusted. The CFO pushed back, the project stalled, and the manual process ran for another two years.

This post is not that slide deck. It is a practical measurement guide for Australian CFOs, finance leaders, and operations managers who want to build an automation ROI case that holds up to scrutiny, survives a board question, and produces documented before-and-after figures after go-live. Every benchmark here is referenced against credible industry data and contextualised for Australian mid-market conditions. Every framework is one you can execute with your existing finance team in a four-week sprint before a single line of automation code is written.

If you want the broader business case structure, the companion post on how to build the finance automation business case covers that ground. This post focuses specifically on measurement: what to track, how to baseline it, what realistic improvement looks like, and where CFOs consistently go wrong when they try to quantify the return.

Key Takeaways

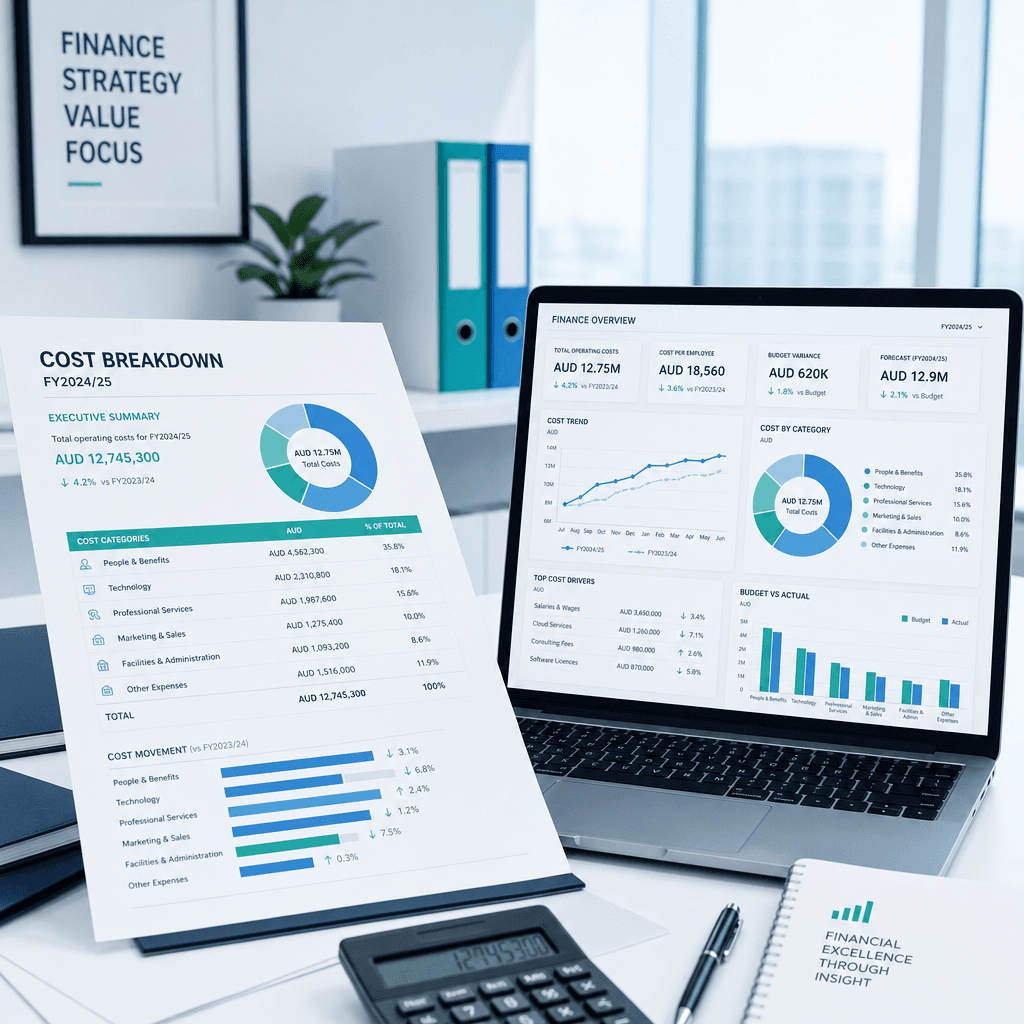

- The five metrics that drive credible finance automation ROI are cost-per-invoice, cycle time, exception rate, FTE hours recaptured, and month-end close duration. Everything else is secondary.

- Australian mid-market organisations process invoices at an average cost of $15-$22 per invoice manually. Best-in-class automated processing costs $2-$4 per invoice. That gap is your primary ROI driver.

- A baseline measurement sprint before go-live is non-negotiable. Without a documented starting point, post-automation numbers are assertions, not evidence.

- Proof-of-concept benchmarks are not ROI benchmarks. The only number that counts is the one measured after go-live against a documented baseline.

- Soft benefits including audit risk reduction, supplier satisfaction, and early payment discount capture are real and quantifiable. Most CFOs undercount them by 30-40 per cent.

- The most common measurement mistake is double-counting FTE savings. Headcount reduction and hours reallocation are different things. Conflating them destroys the credibility of your business case.

- AI-assisted automation consistently outperforms rules-only automation on exception rates, which is the single biggest driver of total processing cost after volume.

Summary Table

| Metric | Pre-Automation Benchmark (AU) | Post-Automation Target | Measurement Method |

|---|---|---|---|

| Cost per invoice processed | $15-$22 | $2-$4 | Total AP team cost divided by invoice volume |

| Invoice processing cycle time | 8-12 business days | 2-3 business days | Date received to date approved, sampled weekly |

| Exception rate (invoices requiring human intervention) | 35-55% | 5-15% | Exceptions logged divided by total invoices |

| FTE hours on manual AP per month | 40-120 hours per FTE | 8-24 hours per FTE | Time-tracked activity logs, 4-week sample |

| Month-end close duration | 7-10 business days | 3-5 business days | Close start to close complete, 3-month average |

| Early payment discount capture rate | 15-25% | 60-80% | Discounts taken divided by discounts available |

| AP coding accuracy | 82-88% | 95-99% | Exceptions attributed to coding errors, monthly |

Why Most Finance Automation ROI Calculations Fail

The failure pattern is consistent. A finance leader attends a vendor demonstration, sees a headline like "reduce AP costs by 80 per cent", builds a business case around that figure, and presents it to the CFO or board. The CFO asks two questions: what is our current baseline cost, and what is the all-in cost of getting from here to there? The finance leader cannot answer either question with confidence, because the baseline was never measured and the vendor projection included none of the implementation, change management, or integration costs.

That business case fails. Not because the 80 per cent is wrong, but because it is unverifiable.

Vanity Metrics vs Actionable Metrics

Vendors and consultants gravitate toward vanity metrics because they produce large, impressive numbers. Total spend under management. Number of invoices processed. Percentage of workflows digitalised. These figures look good in a presentation and are almost impossible to tie to a dollar outcome.

Actionable metrics do the opposite. They are specific, they have a dollar value attached, they can be measured before and after the intervention, and they are defensible under questioning. Cost-per-invoice is an actionable metric. "Digital transformation maturity score" is not.

The distinction matters because boards and CFOs are trained to stress-test numbers. A vanity metric will not survive a single follow-up question. An actionable metric with a documented baseline and a post-go-live comparison can withstand a full audit committee review.

The Baseline Problem

The single most common reason finance automation ROI calculations fail is the absence of a pre-automation baseline. Organisations go live with automation, see improvement, but cannot quantify it because they never measured where they started. They are left saying "things feel faster" rather than "invoice cycle time dropped from 11 days to 2.5 days, which represents $180,000 in recovered capacity annually."

I have seen this pattern repeatedly across the work we have shipped. A manufacturing client came to us having already deployed an OCR tool that had been running for six months. They wanted to know if it was working. They had no pre-automation invoice volume data, no baseline cycle time records, and no historical exception rate. The tool may have been performing well. We had no way to prove it, and neither did they. We had to run a four-week baseline measurement exercise before we could answer the question. That cost them time and created uncertainty they could have avoided entirely.

Baseline measurement is not optional. It is the foundation every other measurement sits on.

The Scope Creep Trap

ROI calculations also fail when the scope of what is being measured drifts during the project. The original business case covers accounts payable automation. By go-live, the project has absorbed procurement approvals, expense management, and a new GL integration. The costs have grown but the measurement framework has not been updated. The ROI looks wrong because it is comparing a narrow benefit case against a broad cost base.

Fix this by locking the measurement scope before the baseline sprint begins. Define exactly which processes are in scope, document the manual cost of those processes only, and hold the post-go-live measurement to the same boundaries.

The 7 Metrics That Actually Matter

After working across eight industries and measuring automation outcomes for clients processing everything from hundreds to tens of thousands of invoices monthly, these are the seven metrics that consistently drive credible, board-ready ROI calculations.

1. Cost Per Invoice Processed

This is the anchor metric for any AP automation ROI case. It combines labour cost, software cost, and error-correction cost into a single per-unit figure that is directly comparable before and after automation.

To calculate it: take the total annual cost of your AP function (salaries, superannuation, software licences, and an overhead loading of 20-30 per cent for office, IT, and management time), divide by the number of invoices processed annually, and you have your current cost per invoice.

Australian benchmarks from the Institute of Finance and Management (IOFM) and Ardent Partners place manual processing costs in the $15-$22 range for mid-market organisations. Best-in-class automated processing at scale achieves $2-$4. For an organisation processing 10,000 invoices annually at $18 per invoice, automation to $3.50 per invoice represents $145,000 in annual savings from this metric alone.

2. Days Payable Outstanding (DPO) Improvement

DPO is the average number of days an organisation takes to pay its invoices. Manual AP processes inflate DPO not because organisations want to pay late, but because invoices sit in queues waiting for human review and approval. The invoice arrives, nobody picks it up for three days, it gets routed to the wrong approver, the approver is travelling, and fourteen days have passed before payment is authorised.

Automation compresses this. Invoices are picked up immediately, matched against purchase orders, and either auto-approved under preset rules or routed to the appropriate human reviewer with all supporting data attached. Cycle time drops from eight to twelve business days to two to three.

For organisations with favourable early payment discount terms, this is where automation ROI can become exceptional. A 2/10 net 30 discount structure (2 per cent discount for payment within 10 days) on $5 million in annual payables is worth $100,000 per year in captured discounts alone. Most organisations with manual AP processes capture fewer than 25 per cent of available early payment discounts. Automation routinely lifts that to 60-80 per cent.

3. Exception Rate

The exception rate is the percentage of invoices that require human intervention before they can be processed. In a manual AP environment, this figure is often close to 100 per cent, because every invoice requires a human to touch it. What actually matters is the rate of exceptions in an automated environment: invoices that the system cannot process without escalating to a human reviewer.

Pre-automation, most organisations do not track this figure at all because every invoice is manually handled. Post-automation, the exception rate becomes the primary measure of system performance and the primary driver of ongoing processing cost.

Ardent Partners benchmarks place exception rates for best-in-class AP teams at below 10 per cent of invoice volume. Mid-market organisations without automation typically see 35-55 per cent of invoices require some form of exception handling, whether that is a missing PO reference, a coding query, or an approval routing error.

For a national manufacturer I worked with, we deployed end-to-end AP workflow covering email intake, OCR extraction, PO matching, and auto-approval under preset rules. Seventy-five per cent of invoices processed automatically with no human touchpoint. That figure represents the inverse of the exception rate: 75 per cent straight-through processing means 25 per cent exception rate, still well above best-in-class but a transformation from the near-100 per cent manual touchpoint baseline.

4. FTE Hours Recaptured

This metric is where the most measurement confusion occurs. Be precise about what you are measuring.

FTE hours recaptured means the number of hours per month your existing finance staff are no longer spending on manual process tasks. It does not automatically mean headcount reduction. It means your existing team has capacity that can be redirected to higher-value work: analysis, business partnering, exception investigation, or month-end close acceleration.

For a logistics client, automation returned more than 160 hours per month to the finance team by eliminating the manual data bridging between their legacy ERP and Xero. Those hours were not translated into redundancies. They were redirected to reconciliation quality review, supplier relationship management, and financial modelling that the team had previously deferred for months.

When presenting this metric to a board, be explicit. State whether you are projecting headcount reduction or capacity reallocation, and present them as separate scenarios with different cost bases. Conflating them is the most common reason a board challenges the labour saving assumptions in an automation business case.

5. Month-End Close Duration

Month-end close time is a composite metric that reflects the efficiency of every upstream process: AP, AR, bank reconciliation, accruals, and intercompany. Automation in any of these areas contributes to close acceleration, but the effect compounds when multiple processes are automated together.

Gartner research places the average month-end close at 6.4 business days for mid-market organisations. Best-in-class organisations close in under 3 business days. The financial value of close acceleration is not always obvious but is substantial: faster close means more accurate period reporting, earlier visibility over results, and reduced overtime for finance staff during close periods.

For a large enterprise finance team processing high monthly invoice volumes across multiple cost centres, we combined RPA with intelligent document understanding to automate coding, PO matching, and routing. The solution achieved greater than 95 per cent coding accuracy and reduced invoice processing time by 65 per cent. The downstream effect on month-end close was a two-day reduction in the time required to finalise AP ledger entries, because fewer exceptions were outstanding at close date.

6. Audit Risk Score

This is a soft metric that most ROI frameworks ignore and most CFOs undervalue. Manual AP processes carry inherent audit risk: duplicate payments, payments without supporting purchase orders, undetected vendor fraud, and inconsistent GST coding. Each of these represents either a direct financial cost or a compliance exposure.

Duplicate payments alone cost Australian organisations an estimated 0.1-0.5 per cent of total AP spend annually, based on IOFM research. For an organisation with $10 million in annual payables, that is $10,000 to $50,000 in recoverable duplicate payments. Automation with systematic duplicate detection eliminates this exposure.

GST coding errors in a manual AP environment are also common and carry ATO audit risk. Automated coding with validation rules applied at the point of data capture reduces miscoding rates significantly and produces a defensible audit trail.

When building the business case, quantify the audit risk reduction conservatively. Use 0.1 per cent of AP spend as your duplicate payment recovery estimate. Add an estimate for the finance staff time spent on audit preparation and reconciliation of manual records. Both are real savings.

7. Supplier Satisfaction and Early Payment Discount Capture

Supplier relationships have a financial value that is rarely included in automation ROI calculations. Slow payment damages supplier relationships, leads to tighter credit terms, and in some cases results in supply disruption. Fast, predictable payment enabled by automated AP processing strengthens supplier relationships and in many cases unlocks preferential pricing or extended credit terms.

Early payment discount capture, as discussed under DPO improvement, is directly quantifiable. Supplier satisfaction improvement is harder to express in dollar terms but is real. Include it in your business case as a qualitative benefit with a conservative dollar range rather than omitting it entirely.

Realistic Australian Benchmarks

Benchmarks drawn from US or European research are not always directly applicable to Australian mid-market conditions. Labour costs, superannuation obligations, the structure of Australian payment terms, and the prevalence of specific ERP platforms all affect what baseline and target figures look like in an Australian context.

Labour Cost Context

ABS data for 2026 places average total employment cost for an accounts payable officer in Australia at approximately $75,000-$90,000 per year including superannuation at the current 11.5 per cent rate. For a senior AP manager, this rises to $100,000-$130,000. These figures are the labour cost base for any FTE hour calculation. Use your actual salary data, but if you are modelling a generic case, these ABS-aligned figures are a reasonable starting point.

Invoice Processing Cost Benchmarks

IOFM's AP benchmarks, contextualised for Australian mid-market conditions by adjusting for local labour costs, place manual invoice processing costs in the following ranges:

- Small organisations (under 500 invoices per month): $20-$28 per invoice

- Mid-market organisations (500-5,000 invoices per month): $15-$22 per invoice

- Enterprise organisations (5,000+ invoices per month): $8-$15 per invoice

Post-automation targets for mid-market Australian organisations:

- With basic OCR and rules-based matching: $5-$8 per invoice

- With intelligent document understanding and AI-assisted coding: $2-$4 per invoice

Cycle Time Benchmarks

Ardent Partners' State of ePayables research, adjusted for Australian payment terms norms (standard 30-day terms versus the 45-60 day terms common in some US sectors), indicates:

- Manual AP cycle time, mid-market: 8-12 business days invoice receipt to payment approval

- Best-in-class automated AP cycle time: 1-3 business days

- Australian mid-market post-automation realistic target: 2-4 business days

Exception Rate Benchmarks

- Manual AP, no automation: 35-55% of invoices require exception handling

- Rules-based automation only: 20-30% exception rate

- AI-assisted automation with learning capability: 8-15% exception rate over time

- Best-in-class (Ardent Partners): below 10%

Month-End Close Benchmarks

- Australian mid-market average (Gartner, contextualised): 6-8 business days

- Post-AP automation target: 4-6 business days

- Full finance process automation target: 2-4 business days

For a detailed breakdown of accounts payable automation specifically, the accounts payable automation guide covers the process architecture behind these benchmark improvements.

How to Baseline Before You Automate

The four-week baseline measurement sprint is the most important work you do before any automation project begins. Skip it and you will not be able to prove your results. Execute it well and you will have everything you need for the business case and the post-go-live evaluation.

Week 1: Volume and Cost Mapping

Start with the numbers that are easiest to pull from your existing systems. You need:

- Invoice volume by month for the past twelve months (seasonal variation matters)

- Total AP team headcount and fully loaded cost

- Software costs for your current AP tools (if any)

- Total AP spend for the period

Divide total AP function cost by invoice volume to get your current cost-per-invoice baseline. Do this for each month and average it. You now have your anchor metric.

Week 2: Cycle Time Sampling

Select a random sample of 50-100 invoices from the past 30 days. For each invoice, record the date received, the date first touched by a human processor, the date sent for approval, and the date approved for payment. Calculate the average cycle time across the sample.

This is not a perfect measurement but it is a defensible one. The sample size is large enough to produce a reliable average and small enough to complete in a week without disrupting normal operations.

Week 3: Exception Rate and Error Tracking

For a fresh 30-day cohort of invoices, ask your AP team to log every instance where an invoice required intervention beyond standard processing. This includes: missing PO references, duplicate invoice flags, coding queries, approval routing errors, and any invoice returned to the supplier for correction.

Count the exceptions, divide by total invoice volume, and you have your exception rate baseline. Also record the average time spent resolving each exception type. This becomes the basis for your exception-cost calculation.

Week 4: Soft Metric Baseline

In the final week, gather the data that will support your softer ROI metrics:

- Run a duplicate payment check across the past twelve months (many AP teams are surprised by what this finds)

- Pull your early payment discount capture rate from your accounts payable ledger

- Survey AP staff on estimated time allocations across task categories

- Check your last three month-end close durations from the finance calendar

By the end of week four, you have a complete baseline. Every metric you will measure post-automation has a documented starting point. This is the difference between an ROI case and an ROI assertion.

If you want a faster way to identify where your baseline is weakest, the finance health check tool gives you a structured view of your current process gaps in under 15 minutes.

Measuring ROI Post Go-Live: The 90-Day Framework

Go-live is not the end of measurement. It is the beginning. The 90-day post-go-live period is when the real ROI story is written, and most organisations do not structure it correctly.

Days 1-30: Stabilisation Metrics

In the first 30 days after go-live, the automation is stabilising. Staff are learning new workflows, exceptions are being tuned, and the system is processing real volume for the first time in production. Do not draw ROI conclusions from this period. Instead, track:

- System uptime and processing reliability

- Exception rate (compare to baseline but expect it to be higher than steady-state)

- Staff adoption rate (what percentage of invoices are being submitted through the new process)

- Issues log (volume and severity of processing errors or workflow failures)

This data tells you whether the automation is stable, not whether it is delivering ROI. Both matter.

Days 31-60: First Performance Window

By day 31, the automation has processed a meaningful volume of invoices and exception tuning has occurred at least once. Now begin measuring against your baseline:

- Cost per invoice (calculate monthly using the same methodology as your baseline)

- Cycle time (run the same 50-100 invoice sample methodology)

- Exception rate (compare directly to baseline)

- FTE hours on manual AP tasks (resurvey staff on time allocations)

Present these figures alongside the baseline with the delta clearly labelled. This is your first ROI data point.

Days 61-90: Full ROI Quantification

By day 90, you have two months of post-go-live data. Average the days 31-60 and days 61-90 figures to smooth out any stabilisation effects. Calculate:

- Annual cost saving extrapolated from monthly cost-per-invoice reduction

- Annual capacity recaptured in FTE hours, valued at fully loaded hourly rate

- Early payment discounts captured in the period (compare to baseline capture rate)

- Duplicate payments detected and recovered

- Exception handling time saved, valued at AP officer hourly rate

Sum these and compare to the total cost of the automation project (implementation, integration, licensing, and change management). That is your ROI.

For organisations using Ordron's automation, every engagement is scoped against specific manual processes with documented baselines, and post-go-live measurement is part of the engagement structure. No aspirational projections: the numbers attached to every piece of work we have shipped are measured after go-live against the baseline we set before we started.

You can also run your numbers through the cost of inaction calculator to see what the manual baseline is costing you in dollar terms while you are still deciding.

AP Automation ROI: A Worked Example Using Australian Figures

Let's build a complete worked example using a realistic Australian mid-market manufacturer. This is a composite, but the figures are drawn from the benchmarks above and from actual engagements.

The Organisation

- Industry: Manufacturing

- Annual revenue: $45 million

- Monthly invoice volume: 1,200 invoices from 180 suppliers

- AP team: 2 FTE AP officers plus 0.5 FTE AP manager

- Current AP technology: MYOB AccountRight, shared Gmail inbox, spreadsheet-based approval tracking

The Baseline (4-Week Measurement Sprint Results)

| Metric | Measured Baseline |

|---|---|

| Cost per invoice | $19.40 |

| Average invoice cycle time | 10.2 business days |

| Exception rate | 48% |

| FTE hours on manual AP per month | 210 hours total |

| Early payment discount capture | 18% of available discounts |

| Duplicate payments in last 12 months | $8,400 |

| Last 3 month-end close durations | 8, 9, 7 business days (avg 8) |

The Automation Scope

Ordron deploys end-to-end AP automation covering: email intake from shared inbox, OCR data extraction with intelligent document understanding, PO matching against MYOB data, auto-approval under preset rules for matched invoices under $5,000, exception routing with context for invoices above threshold or with mismatches, and a live spend dashboard for the AP manager.

Total project cost (implementation, integration, 12 months of licensing): $48,000.

Post Go-Live Results (90-Day Measurement)

| Metric | Baseline | Post-Automation | Improvement |

|---|---|---|---|

| Cost per invoice | $19.40 | $4.20 | 78% reduction |

| Average invoice cycle time | 10.2 days | 2.4 days | 76% reduction |

| Exception rate | 48% | 22% | 54% reduction |

| FTE hours on manual AP per month | 210 hours | 52 hours | 75% reduction |

| Early payment discount capture | 18% | 64% | 256% increase |

The ROI Calculation

Labour cost saving: Hours saved: 158 hours per month x 12 = 1,896 hours per year. At a fully loaded AP officer cost of $42/hour (based on $75,000 fully loaded annual cost / 1,800 work hours), the annual labour saving is $79,632.

Important note: this is expressed as capacity recaptured, not headcount reduction. The 2 FTE AP officers are retained and redirected to supplier relationship management, exception review, and reporting work that was previously deferred.

Processing cost saving: Cost reduction from $19.40 to $4.20 per invoice = $15.20 per invoice. At 14,400 invoices per year, this is $218,880. Note: labour saving is already captured in the cost-per-invoice figure, so to avoid double-counting, express the processing cost saving net of the labour component already counted above. The non-labour component of cost reduction (software, overhead, error correction) accounts for approximately 35 per cent of the total gap, or $76,608.

Early payment discount capture increase: Annual payables: $12 million. Available discounts at average 1.5 per cent on 40 per cent of invoices with discount terms = $72,000 available. Baseline capture (18%): $12,960 captured. Post-automation capture (64%): $46,080 captured. Incremental annual value: $33,120.

Duplicate payment recovery: Baseline: $8,400 per year in duplicate payments. Post-automation: near-zero with systematic duplicate detection. Annual saving: $8,400.

Total annual benefit:

- Labour capacity recaptured: $79,632

- Non-labour processing cost reduction: $76,608

- Early payment discount increase: $33,120

- Duplicate payment recovery: $8,400

- Total: $197,760

ROI calculation: Project cost: $48,000. Annual benefit: $197,760. Payback period: approximately 2.9 months. Year 1 ROI (net of project cost): $149,760 / $48,000 = 312%.

This is a realistic worked example, not a best-case scenario. The numbers sit within the benchmarks cited throughout this post. For a real engagement, your figures will differ based on your invoice volume, labour costs, payment terms, and automation scope. The automation ROI scorecard lets you input your own figures and get a tailored estimate.

You can also see how similar outcomes were achieved for a national manufacturer in the manufacturing invoice hub case study and for a large enterprise AP team in the enterprise AP IDU case study.

Common Measurement Mistakes

Even finance leaders who approach automation measurement seriously make predictable errors. Here are the ones I see most often and how to avoid them.

Mistake 1: Double-Counting FTE Savings

This is the most damaging error in any automation ROI case because it is easily identified by a sceptical CFO or board director. It happens when you count both the hourly labour saving (FTE hours recaptured at hourly rate) and the headcount reduction saving (FTE cost eliminated) as separate line items, when they are the same saving expressed two different ways.

The rule: pick one approach and be explicit. If you are projecting that automation will allow you to reduce AP headcount by one FTE, express the saving as the fully loaded cost of that FTE. Do not also claim the hourly saving for those same hours. If you are projecting capacity reallocation with no headcount reduction, express the saving as the dollar value of redeployed capacity (which is lower than the full FTE cost, because it assumes the person is still employed and the saving comes from not needing to hire additional staff as the business grows).

Mistake 2: Ignoring Change Management Costs

Automation projects that fail to account for change management costs consistently understate the total project investment and therefore overstate the ROI. Change management in a finance automation context includes: staff training time (which has a labour cost), process documentation effort, temporary productivity reduction during the transition period, and management time spent on adoption monitoring.

For a typical mid-market AP automation project, change management costs run at 15-25 per cent of the total technical implementation cost. Include them in the denominator of your ROI calculation.

Mistake 3: Using Vendor Benchmarks Without Localisation

A vendor quoting US cost-per-invoice benchmarks in an Australian business case is using figures that may be 20-40 per cent below Australian equivalents due to lower US labour costs. This understates your current baseline cost, which in turn understates the benefit of automation. Counterintuitively, using accurate Australian benchmarks makes your ROI case stronger, not weaker. Use ABS labour cost data and IOFM figures contextualised for Australian mid-market conditions.

Mistake 4: Measuring at the Proof-of-Concept Stage

A proof of concept that demonstrates the technology works is not an ROI data point. Processing 50 invoices correctly in a sandbox environment tells you nothing about how the system will perform at production volume, how staff will adopt it, or what the true exception rate will be under real-world conditions.

The benchmark is measurable outcomes after go-live, with documented before-and-after figures attached to every engagement. Anything measured before production deployment is a hypothesis, not a result.

Mistake 5: Unrealistic Timeline Assumptions

Vendors commonly quote payback periods of three to six months. These are achievable but depend on implementation timelines, adoption rates, and invoice volumes that may not match your situation. For a mid-market organisation with a structured implementation, a realistic payback period is three to nine months from go-live. Present this range to your board rather than the optimistic single figure.

Mistake 6: Failing to Account for Legacy System Reality

Many Australian mid-market organisations run legacy ERP systems that vendors claim are too old or too limited to integrate with automation tools efficiently. This leads to business cases that include ERP replacement costs alongside automation costs, dramatically inflating the investment and crushing the ROI.

Legacy systems rarely need replacing. Every system your finance team uses has an interface, even if it has no API. RPA can operate that interface the same way a human would, validate the output, and sync clean data downstream. Replacing a working system introduces project risk, retraining cost, and months of delay. Automating around it produces measurable results in weeks, with no disruption to the stack the team already knows.

A logistics operator I worked with had run a twenty-year-old ERP with no APIs alongside Xero for years. Finance staff spent significant time each month manually bridging data between the legacy system and reporting tools, with no reliable way to validate what had transferred correctly. We built an RPA bot that drove the legacy ERP interface directly, validated extracted records against SQL, and synced clean data into Xero and live reporting dashboards without replacing or modifying the ERP. The automation returned more than 160 hours per month to the finance team and eliminated the manual reconciliation layer entirely. No new software, no ERP replacement, no disruption. Just the connective tissue between systems they already owned.

How to Present Finance Automation ROI to a Board

A technically correct ROI calculation can still fail to get board approval if it is presented poorly. Boards evaluate investment proposals through a specific lens: strategic alignment, risk, and return certainty. Your presentation needs to address all three.

Lead With the Problem, Not the Solution

Start with the current state in dollar terms. Show the board what manual AP is costing the organisation per year using the cost-per-invoice baseline calculation. Show the cycle time and its impact on working capital. Show the exception rate and what it costs in staff time to resolve. Make the status quo painful before you introduce the solution.

Present a Range, Not a Point Estimate

Boards are trained to distrust single-point estimates. Present a conservative case, a base case, and an optimistic case for your ROI calculation. Use different assumptions for each, and be transparent about what drives the difference. This demonstrates rigour and gives the board a range to work with rather than a number to attack.

Separate Quantified and Qualified Benefits

Present your hard dollar benefits (cost-per-invoice reduction, FTE capacity recaptured, discount capture increase, duplicate payment recovery) with the full calculation visible. Then present your soft benefits (audit risk reduction, supplier relationship improvement, staff satisfaction) separately, with a conservative dollar range attached where possible. Label them clearly so the board knows which numbers have a calculation behind them and which are estimates.

Address the Legacy System Question Before It Is Asked

If your organisation runs legacy systems, address the integration question proactively. State explicitly that the automation will operate alongside existing systems without replacement, explain the RPA approach, and note that this approach eliminates ERP replacement risk and cost from the investment calculation. Boards ask this question almost every time.

For a deeper dive into building the full business case document, including stakeholder maps and risk registers, see the companion post on how to build the finance automation business case.

If you are ready to scope a project and want to talk through the measurement framework for your specific situation, the contact page is the right place to start.

References

-

Institute of Finance and Management (IOFM), Accounts Payable Benchmarking Report: The IOFM produces annual benchmarking research covering cost-per-invoice, cycle time, exception rates, and staffing ratios for AP operations across North American and global organisations. Figures cited in this post have been contextualised for Australian mid-market labour costs using ABS employment data.

-

Ardent Partners, State of ePayables Annual Report: Ardent Partners' annual research series covers AP performance benchmarks including straight-through processing rates, exception handling metrics, early payment discount capture, and technology adoption across organisations of varying sizes. The best-in-class benchmarks cited in this post are drawn from this research.

-

Gartner, Finance Function Technology and Automation Research: Gartner's finance function research covers month-end close benchmarks, CFO technology adoption trends, and the performance outcomes associated with different levels of finance automation maturity. The 6.4 business day average close figure cited in this post is drawn from Gartner's mid-market benchmarking data.

-

Australian Bureau of Statistics (ABS), Labour Cost and Earnings Data: ABS data on average weekly earnings and employment costs for Australian administrative and financial services occupations provides the labour cost baseline for all FTE cost calculations in this post. Superannuation is applied at the current statutory rate of 11.5 per cent.

-

Levvel Research (formerly PayStream Advisors), AP and Invoice Automation Report: Levvel Research's annual invoice automation survey provides data on automation adoption rates, implementation timelines, ROI realisation periods, and the impact of AI-assisted versus rules-only automation on exception rates and processing accuracy.

Frequently asked questions

- How long does it typically take to see ROI from finance automation in Australia?

- For mid-market Australian organisations implementing AP automation, the most common payback period is three to nine months from go-live. Organisations processing over 1,000 invoices per month with clear baseline data and a structured implementation typically see payback within three to five months. Smaller organisations or those with complex legacy integrations may take six to nine months to reach payback. Any projection shorter than three months from go-live should be treated with scepticism unless the invoice volume and labour cost baseline clearly support it.

- What is the minimum company size or invoice volume to make AP automation ROI positive?

- AP automation becomes clearly ROI positive for Australian organisations processing 300 or more invoices per month. Below that threshold, the implementation cost can be hard to recoup within 12 months unless the organisation has unusually high labour costs or significant early payment discount opportunities. For organisations above 500 invoices per month, full end-to-end AP automation almost always produces a positive ROI within six months at Australian labour cost rates.

- How do I measure soft benefits like staff satisfaction and supplier relationship improvement?

- Soft benefits require a measurement methodology before go-live. For staff satisfaction, run a structured survey before automation and repeat it at 90 days post go-live, asking about time spent on repetitive manual tasks and ability to focus on analytical work. For supplier relationships, track the number of payment queries received from suppliers per month before and after automation. Faster, more predictable payment typically reduces query volume by 40-60 per cent, which is a quantifiable proxy for relationship improvement.

- Is the ROI different for AP automation versus AR automation?

- Yes, the ROI drivers are different. AP automation ROI is primarily driven by processing cost reduction, cycle time compression, and early payment discount capture. AR automation ROI is primarily driven by days sales outstanding reduction, bad debt reduction, and reconciliation time saving. Both produce strong ROI but require separate business cases with separate metrics.

- What role does AI play in improving finance automation ROI compared to rules-based automation alone?

- AI-assisted automation consistently outperforms rules-only automation on exception rate and coding accuracy. Rules-based systems handle invoices that exactly match their programmed conditions. AI-assisted systems can interpret new invoice formats, infer GL coding from context, and learn from corrections. Rules-only AP automation typically achieves 20-30 per cent exception rates. AI-assisted automation targets 8-15 per cent at steady state, significantly reducing exception-handling labour costs over time.

- How should I present finance automation ROI to a sceptical board?

- Present a three-scenario model (conservative, base, optimistic) with clearly labelled assumptions. Lead with the cost of the current state in dollar terms before introducing the automation investment. Separate hard dollar benefits with full calculations from soft benefits with transparent estimates. Address legacy system integration proactively and present payback period as a range rather than a single point estimate. Baseline data from a pre-automation measurement sprint is the most effective evidence you can bring to a board presentation.

- Can I automate finance processes without replacing or upgrading my existing ERP?

- Yes, in almost all cases. RPA can operate any system with a user interface, including legacy ERPs with no API access. Validation rules applied to extracted data ensure accuracy before it is written to downstream systems. Modern AP automation tools integrate with MYOB, Xero, SAP, Oracle, and legacy custom ERPs through API integration where available and RPA where it is not. Organisations can achieve measurable results in weeks working within their existing stack without a costly ERP replacement.

- How do I know if I am getting accurate results from my automation vendor's ROI calculator?

- Check four things: whether the calculator uses Australian labour cost figures rather than US or global averages; whether it includes change management and implementation cost in the denominator; whether the exception rate assumption matches your actual baseline; and whether it extrapolates from production go-live data or demo environment performance. If any of these are unfavourable, adjust the inputs or build your own model using a documented baseline measurement sprint.

Ordron

Finance automation team, Sydney

Ordron builds the finance automation infrastructure that runs AP, AR, reconciliations and reporting on autopilot for Australian mid-market businesses.

More from the Ordron Insights catalogue

Selected by topic. Updated as the agent publishes.

Finance Automation ROI Benchmarks for Australian Businesses: What Good Actually Looks Like

Every vendor selling finance automation will show you a projected ROI slide. The numbers are always impressive: cost savings in the hundreds of thousands,…

How Much Does Finance Automation Cost in Australia? A Pricing Guide for CFOs (2026)

Ask three finance automation vendors for a quote and you will get three completely different answers. One will talk about platform licensing, another will lead…

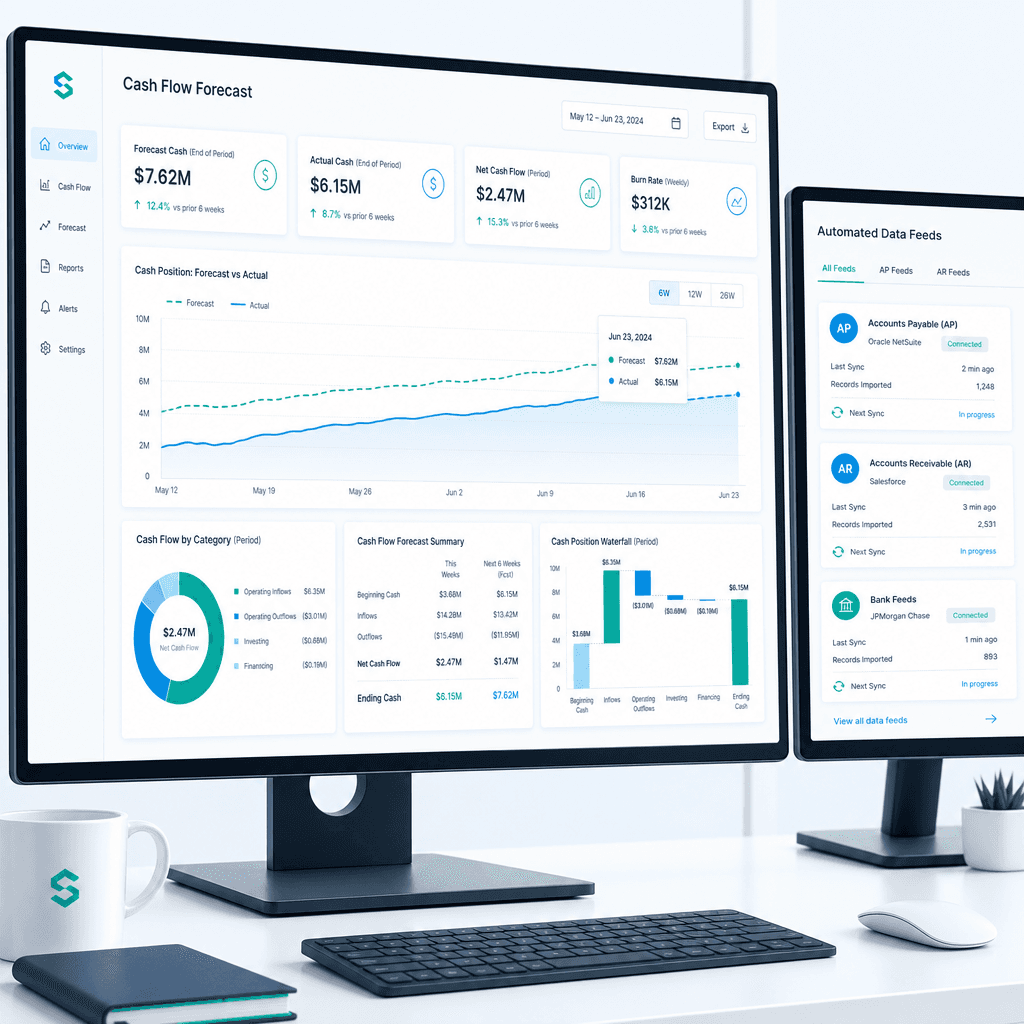

Cash Flow Forecasting Automation: A Practical Guide for Australian Finance Teams (2026)

If your finance team rebuilds the cash flow forecast from scratch every week or every month, you already know where the time goes. Someone pulls an AR ageing…