Finance Automation for Professional Services Firms in Australia: How Accounting, Legal & Advisory Firms Are Streamlining AP, Billing and Reporting

Ordron24 min read

Professional services firms sell time. That is the entire business model. Yet walk into the finance function of almost any accounting, legal or advisory firm in Australia and you will find senior people spending hours each week on manual invoice coding, bank reconciliations, trust account journals and month-end consolidations that could be fully automated. The irony is sharp: firms that bill clients at $300 to $600 per hour are absorbing thousands of dollars of internal cost every month on work a well-configured automation pipeline would handle overnight.

The ABS counts more than 150,000 professional services businesses operating across Australia, many of them carrying finance operations that have not materially changed since Xero replaced their desktop MYOB install. The tools are better, but the processes are still manual, the spreadsheets are still everywhere and the month-end close still runs three to five business days longer than it should. That gap is not a software problem. It is a process and integration problem, and it is exactly the gap automation closes.

This article covers the five finance processes professional services firms should automate first, how legal and advisory firms are already doing it, what platform and compliance considerations matter in an Australian context, and how to assess your own readiness. Everything here is grounded in work we have shipped and the numbers attached to it, not aspirational projections.

Key Takeaways

- Accounts payable automation eliminates manual invoice coding and PO matching, cutting AP cycle times by more than 60% without replacing your existing practice management or accounting platform.

- Trust account automation reduces the risk of compliance breaches under state Law Society and Legal Services Commissioner rules by removing manual journal entries from the reconciliation process.

- Timesheet-to-invoice pipelines remove the lag and errors between WIP capture and client billing, directly protecting revenue.

- Multi-entity consolidation automation collapses month-end reporting from days to hours for firms operating across multiple entities or office locations.

- ATO compliance, BAS lodgement and audit trail requirements are easier to meet when every transaction flows through a structured, logged automation layer rather than a patchwork of manual steps.

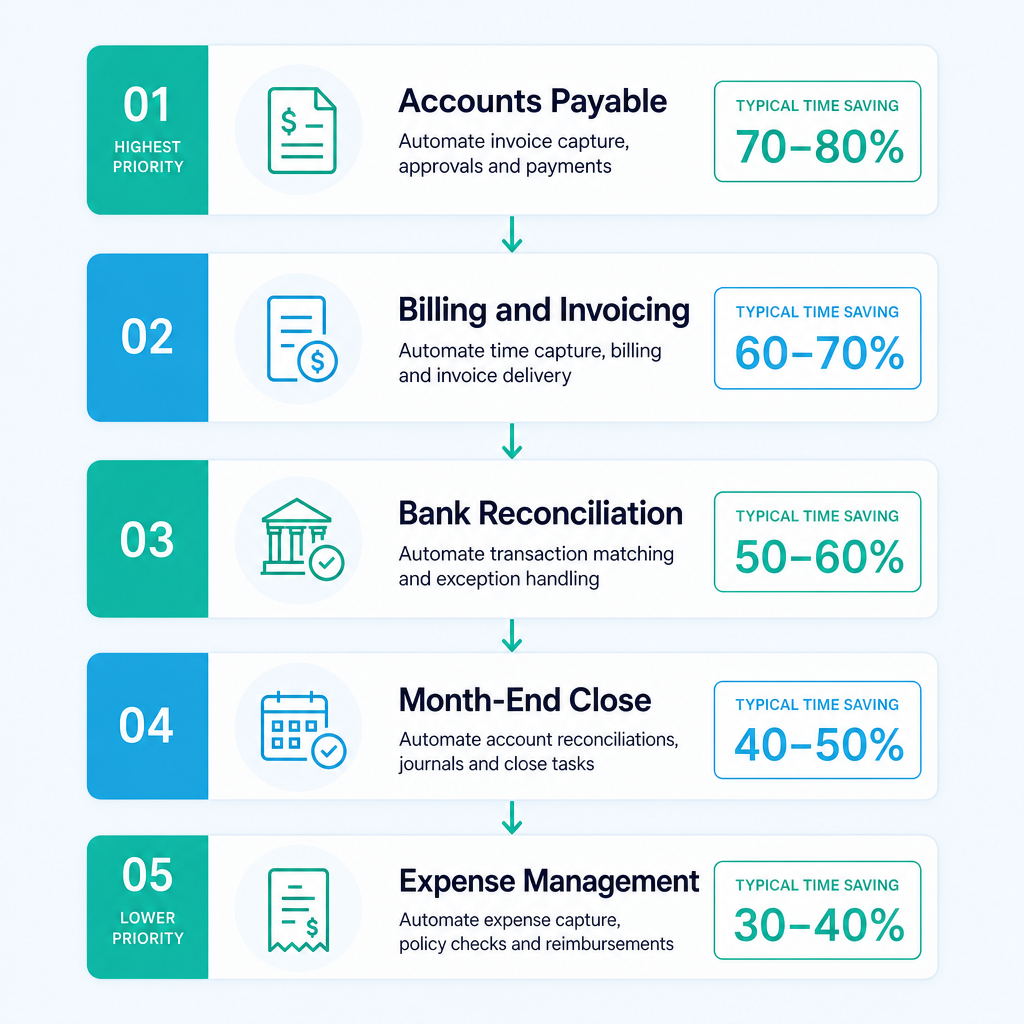

Summary Table

| Process | Manual Pain Point | Automation Solution | Typical Time Saved |

|---|---|---|---|

| Accounts payable | Manual coding, PO matching, approval chasing | Intelligent document understanding, automated GL coding, exception routing | 60-75% reduction in processing time |

| Trust accounting | Manual journals, daily reconciliation risk | Automated reconciliation with audit trail and exception alerting | 70%+ reduction in reconciliation time |

| Timesheet-to-invoice | WIP lag, billing disputes, write-offs | Automated WIP extraction, invoice generation, approval workflow | 50-65% reduction in billing cycle time |

| Month-end consolidation | Excel-based multi-entity rollups, version control chaos | Automated consolidation from source systems into reporting layer | 2-4 days cut from close cycle |

| Expense management | Receipt chasing, manual categorisation, policy checking | OCR capture, automated policy matching, manager approval routing | 80%+ reduction in processing time |

Why Professional Services Firms Face Unique Finance Challenges

Most finance automation content is written with a product or manufacturing business in mind. Professional services firms face a different and, in several ways, harder set of problems.

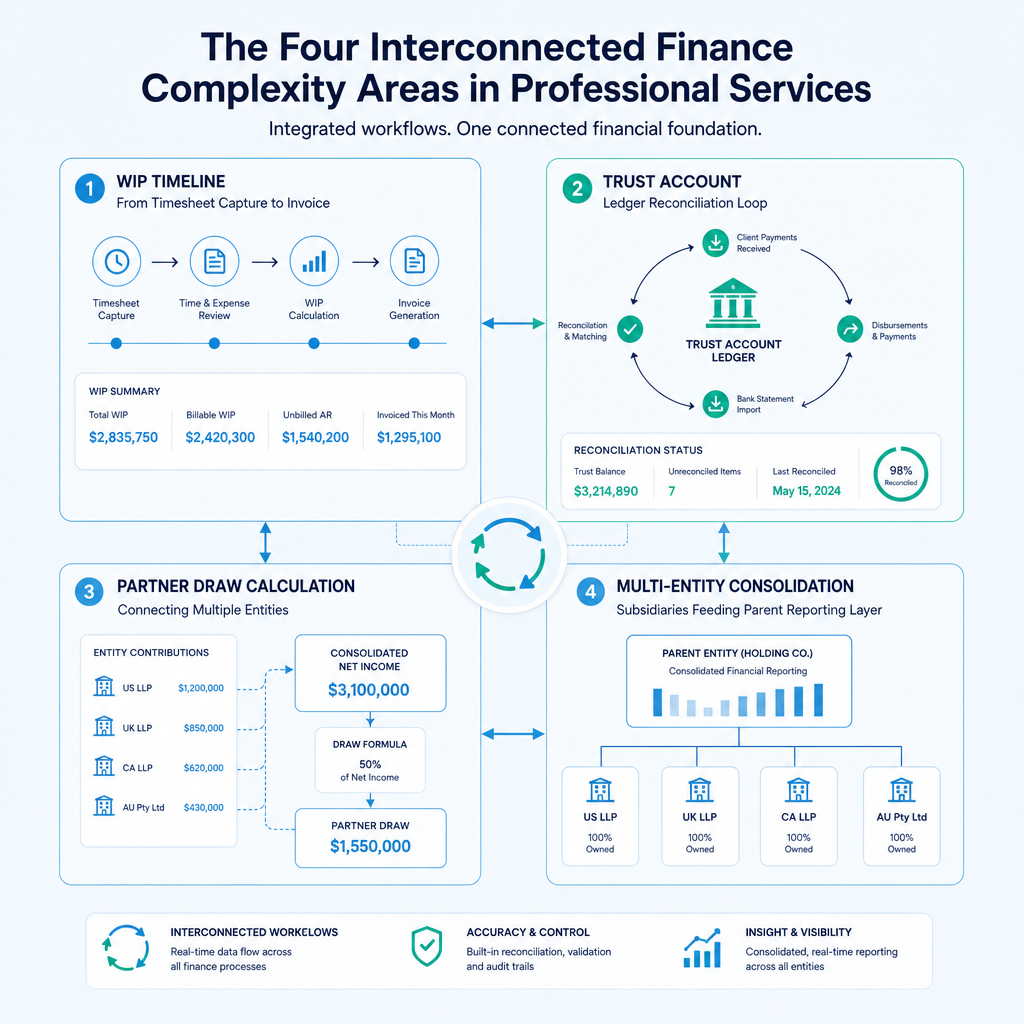

Work in Progress Is Not Inventory

Manufacturing businesses carry physical inventory with a clear dollar value on a shelf. Professional services firms carry WIP: time recorded but not yet billed. WIP is intangible, it is captured through timesheets that practitioners fill in late, and it is adjusted constantly through write-ups and write-downs that reflect negotiated client relationships rather than fixed prices. Automating the path from timesheet to invoice requires integrating your practice management platform (whether that is MYOB Practice, Karbon, GreatSoft or a custom-built system) with your billing engine, and managing the exceptions where a partner has agreed to cap a fee.

The firms that do this well reduce debtor days and write-off rates simultaneously. The firms that do not do this well have a billing team manually extracting WIP from their practice management system into Excel, reformatting it, getting partner sign-off over email and then re-entering it into their accounting platform. I have seen this exact process in firms that bill over $10 million annually and wonder why they are always chasing debtors.

Trust Accounting Is a Compliance Obligation, Not Just a Finance Function

Legal firms operating in Australia hold client money in trust accounts governed by state-based legislation and overseen by the relevant Law Society or Legal Services Commissioner. The obligations are specific: trust receipts must be recorded immediately, reconciliations must be performed at defined intervals, and shortfalls are treated as serious breaches. Manual trust accounting, with human data entry and monthly reconciliations, creates the conditions for error. Automation does not remove the obligation; it removes the manual steps that create risk.

Automated trust account reconciliation connects your trust ledger directly to your bank feed, matches receipts and disbursements in real time and routes only unmatched items to a human reviewer. The reconciliation is no longer a two-hour monthly task performed under deadline pressure. It becomes a daily background process that flags exceptions the moment they occur.

Partner Draws and Multi-Entity Structures Create Consolidation Complexity

Many mid-size accounting and advisory firms operate across multiple entities: a services trust, a corporate trustee, an operating company and sometimes separate entities for different practice lines. Partner draw calculations often depend on data sitting across several of these entities. Month-end consolidation in this environment, done manually, means someone is opening six Xero organisations, exporting data to Excel, eliminating intercompany transactions by hand and hoping the version they send to the managing partner is the one they actually reconciled.

This is the kind of problem that automation solves cleanly. A properly built consolidation layer pulls from all source entities, applies the intercompany elimination rules and produces a consolidated P&L and balance sheet without a human touching a spreadsheet. The process that used to consume two full days of a senior accountant's time runs overnight.

5 Finance Processes to Automate First

Not every automation is worth the same investment. Here are the five areas where professional services firms consistently see the fastest return.

1. Accounts Payable

AP is the most mature automation use case and the one where the numbers are clearest. Supplier invoices arrive by email, get manually opened, coded to the correct GL account and cost centre, matched to a purchase order if one exists, routed for approval and then entered into the accounting system. Every one of those steps except the approval decision itself is automatable.

Intelligent document understanding reads the invoice, extracts the supplier name, invoice number, line items, amounts and GST, matches it against open purchase orders and codes it to the GL based on supplier rules or machine-learning classification. Exceptions, invoices that do not match a PO or that fall outside coding rules, are routed to a human reviewer. The rest post automatically.

In one engagement I ran with a large enterprise finance team processing high monthly invoice volumes across multiple cost centres, we deployed RPA combined with intelligent document understanding. The result was greater than 95% coding accuracy and a 65% reduction in invoice processing time. Human effort was reserved for edge cases only. That is not a projection. That is a measured outcome after go-live.

For professional services firms, AP automation is particularly high value because the people doing manual invoice coding are usually qualified accountants who should be doing higher-value work. Returning those hours to the business is not a marginal win.

2. Billing and Invoicing

The billing cycle in most professional services firms goes: extract WIP from practice management, review with fee earner or partner, write off or write up as agreed, generate draft invoice, get partner approval, send to client. Every handoff in that chain is a delay, and delays in billing directly affect cash flow.

Automating the billing cycle means building an integration between your practice management system and your accounting platform so that WIP is extracted automatically on a defined schedule, draft invoices are generated based on billing rules (fixed fee, time and materials, or capped fee with override flag), approval workflows run through a structured channel rather than email, and issued invoices flow directly into the AR module without re-entry. The firms that have automated this process reduce their average debtor days because invoices go out faster and more consistently.

3. Bank Reconciliation

Bank reconciliation is the manual finance task that most firms have partially automated through bank feeds in Xero or MYOB, but partially is the operative word. Bank feeds bring transactions in automatically; matching them to transactions in the ledger still requires human review in most practices, particularly where clients pay in batches, where trust account transactions need to be matched to matter ledgers, or where the firm uses multiple bank accounts across entities.

Full bank reconciliation automation applies matching rules based on amount, reference, counterparty and date, and routes only genuinely ambiguous items to a human. Across engagements, we have seen AR reconciliation time drop by 80% in firms with large recurring client bases. You can read more about the mechanics in our reconciliation automation guide.

4. Month-End Close

Month-end close is the finance process that most reliably consumes more time than anyone budgets for, and in professional services firms the problem compounds because the data is spread across practice management systems, trust accounting modules, billing platforms and accounting software that may or may not integrate natively.

Automating month-end means building a structured close checklist that is executed by automation rather than by a person walking through a spreadsheet. Intercompany transactions are eliminated automatically. Prepayments and accruals are posted based on scheduled rules. WIP is cut off at month end. Consolidated reports are generated from source data and distributed to partners without manual intervention. Our month-end close automation guide covers the full close sequence in detail.

5. Expense Management

Expense management is often the last finance process to get attention, which is ironic because it is one of the most visible to the people experiencing it. Partners and senior staff submit expense claims with receipts, a finance team member manually reviews them against policy, codes them to the right matter or cost centre, and enters them into the accounting system. In firms with travelling professionals or client entertainment budgets, this process runs every fortnight and absorbs hours.

OCR-based capture reads receipts from a mobile photo, intelligent classification categorises the expense type, policy rules flag anything that exceeds limits or falls into excluded categories, and approved expenses post directly to the GL and the correct matter code. The finance team sees only policy exceptions.

How Legal Firms Are Using AI Contract and AP Automation

Legal firms face an interesting automation opportunity that goes beyond the finance function into the documents that drive the finance function. Engagement letters, retainer agreements and disbursement arrangements are all documents that contain billing information, scope definitions and payment terms. When those documents are processed manually, the finance team is dependent on fee earners to communicate billing arrangements accurately. When they are processed through an intelligent document pipeline, the finance system can read the terms directly.

Our legal AI contracts case study details exactly how one Australian legal firm used AI-powered document understanding to extract billing terms from engagement letters and feed them directly into their billing workflow, removing a manual handoff that had been causing billing discrepancies for years. The AP side of the same engagement automated supplier invoice processing for the firm's operating expenses, integrating directly with their existing practice management and accounting environment without introducing new software.

The trust accounting dimension for legal firms deserves specific attention. State-based trust accounting rules in Australia, including the requirements under the Legal Profession Uniform Law in NSW and Victoria and equivalent legislation in other states, require meticulous record-keeping. Automated reconciliation with a complete audit trail is not just an efficiency gain for legal firms. It is a meaningful risk reduction.

Advisory Firm Case Study: From Excel to Enterprise Reporting

For accounting and advisory firms, the move from manual Excel-based reporting to automated enterprise consolidation is one of the highest-leverage automations available. Our advisory firm case study walks through how a mid-size Australian advisory firm eliminated a consolidation process that had been running in Excel for over a decade.

The firm operated across four entities with a shared services structure. Month-end consolidation required a senior accountant to spend approximately two full days extracting data from each entity's Xero organisation, building an intercompany elimination schedule, and populating a reporting template. The process was prone to version control errors and depended entirely on one person's availability.

Ordron built an automated consolidation pipeline that connected to all four Xero organisations, applied the intercompany elimination rules and produced a consolidated report set in a structured reporting layer. The two-day manual process became an overnight automated run. The senior accountant's time was redirected to analysis and partner advisory, which is where a firm of that calibre should be deploying qualified people.

This is also worth reading alongside our financial services risk AI case study and PE analytics case study, which illustrate how firms at the more complex end of the market are extending automation from transactional processing into analytical and risk workflows.

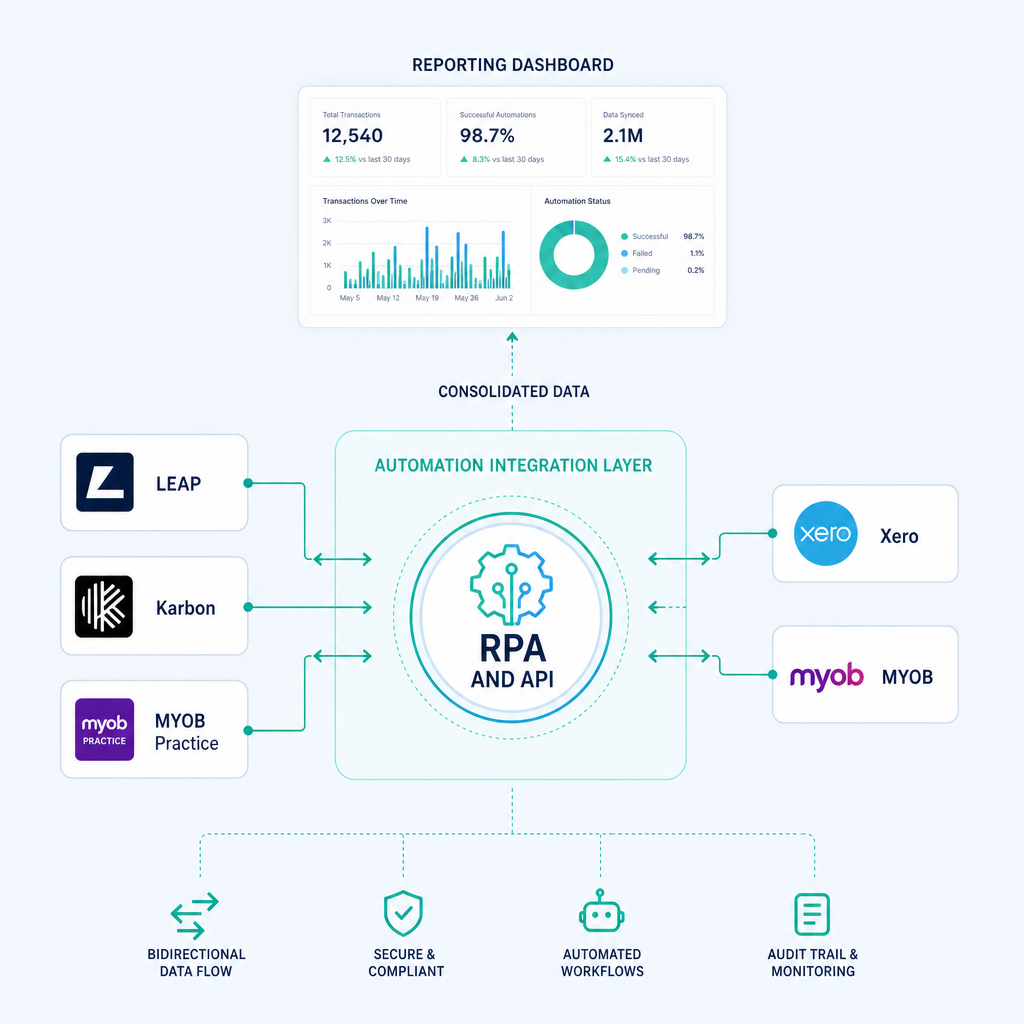

Platform Considerations: Xero, MYOB and Practice Management Integration

The most common question I get from professional services firm leaders considering automation is whether they need to change their accounting platform or practice management system first. The answer is almost always no.

The premise that you need modern, API-ready systems before automation can deliver results is one I actively disagree with. The logistics operator I mentioned earlier ran a twenty-year-old ERP with no APIs alongside Xero. Rather than recommending a platform replacement, we built an RPA layer that drove the legacy ERP interface directly, validated the data and synced clean records into Xero and the reporting dashboards. The result was over 160 hours per month returned to the business, without replacing the ERP. The system was never the problem. The lack of integration between systems was the problem.

For professional services firms, the platforms that matter most are:

Xero is the dominant cloud accounting platform for Australian professional services firms and has strong API support. Automation built on top of Xero can handle everything from AP posting to bank reconciliation matching to consolidated reporting. See our Xero automation platform page for the specific integration patterns we deploy.

MYOB remains common in mid-market accounting and legal firms, particularly those that have been operating for more than fifteen years. MYOB AccountRight and MYOB Advanced both have API access, though the depth varies. Where API access is limited, RPA can bridge the gap without a platform migration.

Practice management platforms vary significantly by profession. Legal firms commonly use LEAP, Actionstep or Smokeball. Accounting firms use Karbon, MYOB Practice, GreatSoft or Xero Practice Manager. Advisory firms often run a combination. The key is that automation sits above these platforms, pulling and pushing data through APIs or RPA rather than requiring you to standardise on a single vendor.

The integration design question is not which platform you use; it is which data needs to flow where and whether that flow is currently manual. Every manual data transfer between systems is an automation candidate. Map those flows first, then assess whether API integration or RPA is the right mechanism for each.

Compliance: ATO, Trust Account Rules and Audit Trails

Automation in professional services finance operates in a compliance-heavy environment. Three areas deserve specific attention.

ATO Obligations

The ATO's requirements for record-keeping, BAS lodgement and tax reporting apply to every Australian business, but professional services firms carry additional obligations as registered tax agents and BAS agents under the Tax Practitioners Board (TPB). The TPB's Code of Professional Conduct requires registered practitioners to maintain systems that ensure the accuracy of their own financial records, not just client records. Automated financial processes, provided they are properly logged and auditable, make compliance with these obligations more reliable, not less.

GST coding accuracy in AP automation is directly relevant here. When invoices are miscoded, GST claims are wrong. When invoices are coded at greater than 95% accuracy through intelligent document understanding and exceptions are reviewed by a human, GST compliance is materially better than in a manual process where a fatigued data entry person is coding 200 invoices at end of month.

Trust Account Rules

Australian legal firms are subject to trust accounting rules that vary by state but share a common structure. The Law Society in each state publishes detailed guidance. In NSW, the Legal Profession Uniform Law and the Legal Profession Uniform General Rules 2015 set out the reconciliation and record-keeping obligations. In Victoria, equivalent obligations apply under the Legal Profession Uniform Law Application Act 2014. The common requirement is that trust account reconciliations must be performed monthly as a minimum, with records maintained for a defined period.

Automated reconciliation, where the system matches every trust receipt and disbursement against the bank statement daily and logs the match result, provides a more defensible compliance record than a monthly manual reconciliation. The audit trail is complete, timestamped and not subject to human memory about why a particular journal was posted.

Audit Trails in Automated Systems

A concern some firms raise about automation is that it removes the human paper trail. The opposite is true when automation is built correctly. Every action performed by an automated process should be logged: what data was read, what rule was applied, what was posted and when, and what was routed to a human and why. That log is a better audit trail than a folder of printed invoices with handwritten approval signatures.

When the ACCC or ATO or a Law Society auditor asks for transaction records, a structured automation log with full provenance is easier to produce and more complete than manual records. This is a governance argument for automation that finance leaders in professional services often overlook.

How to Get Started: Readiness Assessment

The most common mistake firms make when starting a finance automation programme is beginning with the technology rather than the process. Before selecting a platform or a vendor, the useful questions are:

- Which finance processes are currently consuming the most time per month, and what is the dollar cost of that time at the loaded hourly rate of the people doing it?

- Where do errors most frequently occur, and what is the downstream cost of those errors (write-offs, compliance risk, debtor disputes)?

- Which of those processes involve repetitive, rule-based steps that a human is performing the same way every time?

- What systems hold the source data for those processes, and do those systems have API access or are they interface-only?

The answers to those four questions define your automation roadmap. The highest priority candidates are the processes with the largest time cost, the highest error risk and the most clearly defined rules. AP coding, bank reconciliation and timesheet-to-invoice pipelines almost always appear at the top of that list for professional services firms.

If you want a structured way to work through this assessment, our finance automation scorecard takes you through the key dimensions and gives you a prioritised view of where automation will deliver the fastest measured return. You can also explore the broader finance automation Australia resource for context on how these programmes are structured across different industries.

One principle I hold firmly: every engagement Ordron runs begins with a commitment to measure outcomes after go-live. No aspirational projections appear in our proposals, and no case study is published until the before-and-after number is confirmed. The anonymised outcomes across industries that I reference in this article come from that discipline. If a vendor cannot tell you what they measured after the last three engagements they shipped for similar firms, that is worth noting.

The gap between a professional services finance team drowning in manual work and one running cleanly is almost never about the software. It is about connecting what you already own in a way that removes the human from low-judgement repetitive tasks and routes only genuine exceptions to people who are qualified to make decisions. That is the work, and the return on it is measurable from day one of go-live.

References

-

Australian Bureau of Statistics, Counts of Australian Businesses (Professional, Scientific and Technical Services), ABS catalogue providing industry counts and structure data for the professional services sector, used to contextualise the scale of the market and the prevalence of small to medium operators carrying manual finance processes.

-

Australian Taxation Office, Record Keeping for Small Business and Tax Practitioners, ATO guidance covering record-keeping obligations for businesses and registered tax agents, relevant to GST coding accuracy, BAS reconciliation requirements and the standards automated systems must meet.

-

Tax Practitioners Board, Code of Professional Conduct, TPB guidance setting out the obligations of registered tax agents and BAS agents, including requirements to maintain systems that ensure the accuracy of returns and reports lodged on behalf of clients and for the firm's own financial records.

-

Law Society of NSW, Trust Accounting Guide, Detailed guidance from the Law Society of NSW on trust account obligations under the Legal Profession Uniform Law, including reconciliation frequency, record retention periods and the requirements for trust receipt and disbursement records.

-

ACCC, Record Keeping and Compliance, ACCC guidance on business record-keeping obligations relevant to audit trail requirements, particularly for firms subject to consumer law compliance as part of their professional services operations.

-

Xero, API Documentation and Partner Integration Guide, Xero's technical documentation for third-party integrations, used to contextualise the API capabilities available to firms building automation on top of Xero's accounting platform in the Australian market.

Frequently asked questions

- What is finance automation for professional services firms?

- Finance automation for professional services firms refers to the use of software, robotic process automation (RPA) and intelligent document understanding to eliminate manual steps in finance processes including accounts payable, billing, bank reconciliation, trust accounting, expense management and month-end reporting. The goal is to remove repetitive, low-judgement tasks from qualified staff so they can focus on higher-value work and client delivery.

- How long does it take to implement AP automation in an Australian accounting or legal firm?

- A focused AP automation deployment for a professional services firm typically takes between four and ten weeks, depending on the complexity of the existing systems, the number of supplier types and whether a purchase order matching layer is required. Firms with clean Xero or MYOB environments and a defined supplier list sit at the lower end of that range. Firms with legacy practice management systems or complex multi-entity structures sit at the higher end. The key variable is data quality in the source systems, not the automation build itself.

- Do we need to replace our practice management system before automating finance processes?

- No. Automation is most valuable when it bridges the systems you already own rather than requiring you to replace them first. RPA can drive legacy interfaces that have no API access, and integration layers can connect practice management platforms, accounting software and reporting tools without requiring a rip-and-replace project. The automation sits above your existing systems and connects them. Replacing your core platform before automating adds cost, risk and delay without changing the underlying process problem.

- How does trust account automation work for Australian legal firms?

- Trust account automation connects your trust ledger to your bank feed, applies matching rules to reconcile receipts and disbursements in real time, and logs every matched and unmatched item with a full audit trail. Unmatched items are flagged immediately for human review rather than sitting undetected until the end-of-month manual reconciliation. This aligns with the reconciliation and record-keeping obligations under state-based legal profession legislation, including the Legal Profession Uniform Law in NSW and Victoria, while significantly reducing the manual effort involved in staying compliant.

- What Australian accounting platforms work best with finance automation?

- Xero is the most commonly automated platform for Australian professional services firms because of its well-documented API and strong adoption across accounting, legal and advisory sectors. MYOB AccountRight and MYOB Advanced also support automation, though the API depth varies by version. Where API access is limited in any platform, RPA bridges the gap without requiring a platform upgrade. Practice management platforms including Karbon, LEAP, Actionstep and MYOB Practice can all be integrated into automated finance workflows through a combination of API and RPA methods.

- How do we measure ROI on finance automation in a professional services firm?

- The most direct ROI measures are hours per month returned to finance and fee-earning staff, reduction in error rates that require rework, reduction in debtor days from faster billing cycles and reduction in compliance risk exposure from improved audit trails. Calculate the loaded cost per hour of the people currently performing the manual tasks, multiply by the hours returned, and set that against the implementation and ongoing licence costs. Across Ordron's engagements, professional services firms have seen AP processing time cut by 60-75%, AR reconciliation time reduced by 80% and month-end close shortened by two to four days. These are post-go-live measurements, not projections.

- Is finance automation suitable for smaller accounting or advisory firms?

- Yes, though the priority processes differ by firm size. For smaller firms (under ten staff), the highest-value automations are typically AP coding, bank reconciliation and expense management, which are the most time-intensive relative to firm size. For mid-size firms operating across multiple entities or with significant trust accounting obligations, consolidation and trust reconciliation automation deliver the largest returns. The important caveat is that a firm needs sufficient transaction volume for automation economics to make sense. A firm processing fewer than 50 supplier invoices per month will see a smaller absolute return than one processing 500, though the percentage time saving is comparable.

- What are the ATO compliance implications of automated financial reporting?

- Automated financial reporting, when built with proper audit trails and logging, supports rather than complicates ATO compliance. Every automated transaction should carry a record of the rule applied, the data source and the timestamp, which makes BAS reconciliation and tax record-keeping more defensible than manual processes. The TPB's Code of Professional Conduct requires registered tax agents to maintain systems that ensure accuracy, and well-built automation meets that standard. The critical requirement is that exception routing works correctly: any item the system cannot classify with confidence must be reviewed by a qualified person before it is posted.

Ordron

Finance automation team, Sydney

Ordron builds the finance automation infrastructure that runs AP, AR, reconciliations and reporting on autopilot for Australian mid-market businesses.

More from the Ordron Insights catalogue

Selected by topic. Updated as the agent publishes.

Cash Flow Forecasting Automation: A Practical Guide for Australian Finance Teams (2026)

If your finance team rebuilds the cash flow forecast from scratch every week or every month, you already know where the time goes. Someone pulls an AR ageing…

Purchase Order Automation: A Practical Guide for Australian Finance Teams (2026)

If your finance team is still raising purchase orders in a shared inbox, chasing approvals over email, and manually matching invoices line by line before month…

Finance Automation Buyer's Guide for Australian Finance Teams: How to Choose, Scope & Measure Automation That Delivers (2026)

Most finance automation buying decisions are made the wrong way. Teams evaluate vendors on feature lists, watch polished demos, and sign contracts based on…